It states that since the liquidity measures were implemented by the agency in June 2025, the active interest rate of multiple banks decreased by 171 basis points, while the passive rate decreased by 335 basis points, stabilizing at 13.28% and 6.28%, respectively, as of March 2026

SANTO DOMINGO.- The Central Bank of the Dominican Republic (BCRD) presented this Wednesday the financial conditions of the nation, in the face of a turbulent international environment, characterized by high volatility and uncertainty as a result of the armed conflict in the Middle East.

The analysis by the governing body shows how bank interest rates continue to be influenced downwards by the liquidity provision measures to the financial system implemented since June 2025 for RD$81 billion, as well as by the accumulated reduction of 50 basis points in the monetary policy rate (MPR), and whose analysis takes as a starting point the month of May 2025, prior to the adoption of the aforementioned measures.

The statement establishes that the interbank interest rate fell from 11.54% in May 2025 to 7.84% in March 2026, a reduction of 370 basis points, after stating that this behavior demonstrates the effectiveness of the monetary policy transmission mechanism in a context where liquidity conditions were ample and boosted by the aforementioned easing measures.

The Central Bank explains that the functioning of the monetary transmission mechanism has significantly influenced the passive interest rate of the financial system. "In the case of multiple banks, this rate decreased by 335 basis points, falling from 9.63% to 6.28% in the period from May 2025 to March 2026. Similarly, the passive rate of savings and loan associations, the second largest subsector in the financial system, fell from 8.73% to 6.35% during the same period, accumulating a decrease of 238 basis points," it emphasizes.

Decrease in active interest rates

The agency points out that this reduction in the passive interest rate has contributed to a significant decrease in the active interest rate of the financial system, facilitating more favorable monetary conditions for credit. It indicates that the average active interest rate of multiple banks fell from 14.99% in May 2025 to 13.28% in March 2026, a decrease of 171 basis points. It adds that a similar trend is observed in savings and loan associations, where this rate adjusted downward by 211 basis points.

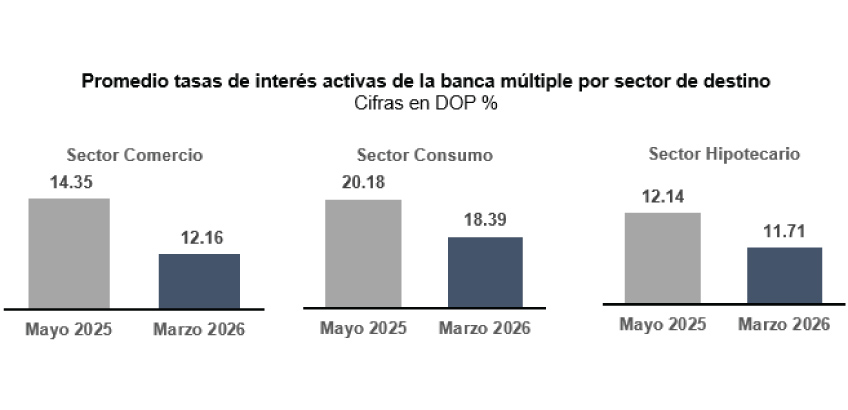

Behavior in the productive sectors

The behavior of the interest rate by economic sector reveals significant decreases in loans granted by commercial banks, encompassing both productive sectors and consumer financing, the Central Bank specifies, noting that it fell from 14.35% in May 2025 to 12.16% in March 2026. "Specifically, in March 2026 the active rate for wholesale and retail trade shows a decrease of 274 basis points compared to the level recorded in May 2025, falling from 14.84% to 12.10%." In the case of the agricultural sector, the active rate was lower by 263 basis points, going from 15.94% in May 2025 to 13.31% in March 2026. At the same time, the active rate of the manufacturing sector registered a decrease of 190 basis points, going from 13.15% in May 2025 to 11.25% in March 2026,” he emphasizes.

Meanwhile, loans to the construction experienced a significant reduction of 253 basis points in the interest rate, going from 14.77% in May 2025 to 12.24% in March 2026.

Regarding personal consumer loans granted by commercial banks, the interest rate fell from 20.18% in May 2025 to 18.39% in March 2026, a decrease of 180 basis points. Meanwhile, the interest rate for loans intended for home fell from 12.14% in May 2025 to 11.71% in March 2026.

Source: Central Bank of the Dominican Republic.

The body emphasizes that the implemented measures achieved a generalized reduction in the financial market interest rate, stabilizing it at levels below those projected for 2025. "These favorable financial conditions have enhanced the performance of the Dominican financial system, which has demonstrated marked strength in terms of liquidity, profitability, and solvency.".

Financial system grows

The Central Bank reports that, according to information from March 2026, the financial system has net assets (after provisions) of RD$4.28 trillion, exhibiting a year-on-year growth rate of 9.2%, similar to the 9.2% year-on-year growth observed for credit to the private sector in local currency, which is higher than the nominal growth of the economy. Furthermore, as a result of profit conversion, the system's capital and equity reserves reached RD$408 billion, representing an expansion of approximately 14.0% year-on-year.

It adds that the delinquency rate of the financial system in March 2026 was 1.8%, that is, 1.8 pesos of overdue loans for every 100 pesos of loans granted, which confirms the improvement in the payment behavior of debtors and in the performance of the loan portfolio by maintaining delinquency levels below 2% after exceeding that threshold in mid-2025.

Levels below 2025

According to the Central Bank, stabilizing the interest rate at levels lower than those observed in 2025 has eased the financial burden on businesses and households, as loans granted with high interest rates have been restructured at a lower financial cost for borrowers. "In a context of increased global instability, this will foster an environment of certainty for macroeconomic stability, reinforcing the customary resilience of the productive sectors, while the Central Bank remains vigilant regarding the international situation in order to act promptly to maintain the inflation target and macroeconomic stability, consistent with its objective of ensuring price stability.".

Recommended readings: